In an age where the internet has blurred borders, two lifestyles have captured the imagination of ambitious people across Africa and beyond — digital nomads and migrants. Both seek better opportunities, freedom, and financial growth, but their paths couldn’t be more different. One lives on flexibility and remote income, while the other seeks stability and new beginnings abroad.

But here’s the big question: Which lifestyle actually saves you more money in the long run?

Let’s break it down.

Understanding the Two Lifestyles

A digital nomad is someone who earns remotely, often through freelancing, remote jobs, or online businesses, while traveling or living temporarily in different countries. They usually rely on Wi-Fi, laptops, and flexible schedules.

A migrant, on the other hand, relocates to another country — usually for education, work, or permanent settlement. They often have to go through visa processes, rent long-term housing, and adapt to local systems like healthcare, taxes, and social services.

Both groups want financial freedom and a better quality of life. However, the way they spend and save money varies dramatically.

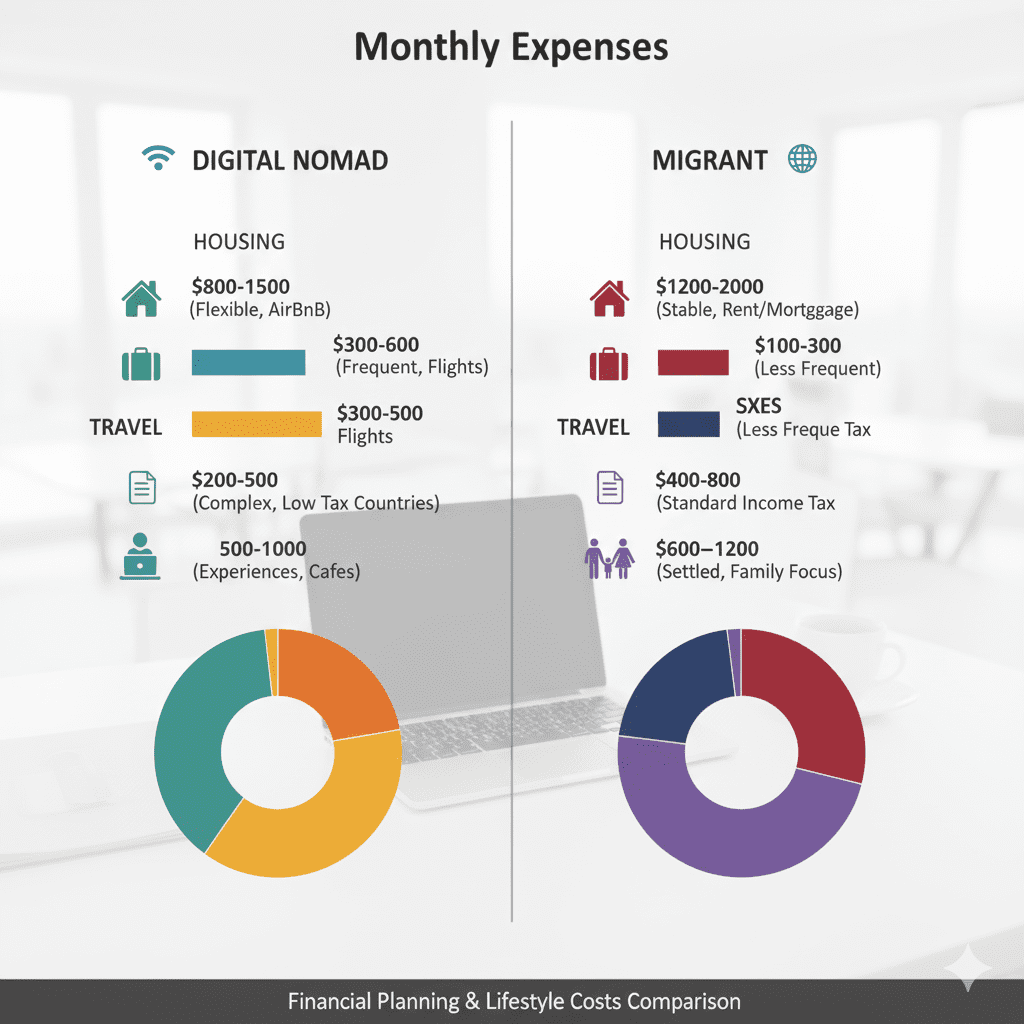

The Cost of Getting Started

For digital nomads, the startup costs are relatively low. You need a good laptop, strong internet connection, and perhaps a few software subscriptions. You can begin freelancing or working remotely from anywhere — even before you travel.

Migrants, on the other hand, face high upfront expenses. Visa fees, travel tickets, relocation costs, housing deposits, and sometimes mandatory proof of funds can quickly add up. A student migrating to Canada or the UK, for instance, may need thousands of dollars before even stepping on the plane.

So in the beginning, digital nomads clearly spend less. They can start small, earn as they go, and relocate when it’s financially convenient. Migrants often have to spend heavily before they start earning.

Living Expenses: Flexibility vs Stability

Digital nomads thrive on flexibility. They can choose to live in affordable destinations like Bali, Mexico, Portugal, or Cape Town, where rent and daily costs are far lower than in major cities like London or Toronto. Many practice “geoarbitrage,” earning in strong currencies like the dollar or euro but spending in cheaper economies.

Migrants, however, are tied to one location. Even if the local cost of living is high, they must adjust. Rent, utilities, and transportation often take a big bite out of their income. A nurse in the UK or student in Canada may find that despite a decent paycheck, savings are difficult once bills and taxes are paid.

This makes the digital nomad lifestyle more cost-efficient in terms of day-to-day living. Flexibility allows them to move where their money stretches further.

Taxes and Financial Responsibilities

Here’s where things get interesting. Digital nomads often work remotely for foreign clients, which means they can legally minimize taxes depending on where they’re based. Many countries offer digital nomad visas with tax benefits or exemptions for a limited period.

Migrants, however, must pay local taxes, contribute to national insurance, and sometimes even double taxation depending on their home country’s laws. While they enjoy the benefits of stable residency, the financial obligations can be significant.

That said, the migrant lifestyle offers long-term financial structure — access to loans, credit systems, and social services that nomads may not qualify for. Digital nomads, in contrast, often face unstable income and limited access to financial systems like mortgages or retirement funds.

Income Stability

One of the biggest challenges for digital nomads is inconsistent income. Freelancers and remote workers sometimes experience slow months or late payments. Managing finances requires discipline and good budgeting.

Migrants who find formal jobs abroad, however, usually enjoy steady income, employee benefits, and predictable expenses. This stability helps them plan better but also ties them to a single income source.

In essence, nomads have flexibility but risk, while migrants have security but higher living costs.

Hidden Costs People Don’t Talk About

Digital nomads often overlook the costs of travel insurance, short-term rentals, visa renewals, and co-working spaces. Constantly moving means higher transportation expenses and limited access to affordable healthcare.

Migrants face hidden costs too — expensive international money transfers, taxes on remittances, and fees for visa renewals or dependents. Many also spend more to maintain ties back home through remittances and family support.

In both cases, financial discipline is essential. The difference lies in how predictable these costs are. Nomads face variable costs depending on their travel patterns, while migrants deal with fixed costs tied to their new home country.

Saving Potential

When it comes to saving money, digital nomads often have the upper hand if they plan well. Earning in dollars and spending in low-cost regions can multiply savings. For instance, a nomad earning $2,000 monthly and living in Thailand can save more than a migrant earning $4,000 monthly in London.

However, migrants can build wealth over time through structured systems — job benefits, retirement savings, and home ownership. A digital nomad’s income may grow faster, but without consistent saving habits, it’s easy to spend impulsively while moving around.

The key difference lies in financial mindset. Migrants tend to think long-term, while nomads think in flexible, short-term goals. Both can save money — but the one who plans strategically wins.

So, Which Lifestyle Saves You More Money?

The answer depends on your goals and discipline.

- If your goal is to save fast and live affordably, the digital nomad lifestyle offers incredible financial advantages. You can earn in strong currencies and live cheaply abroad while keeping expenses minimal.

- If your goal is long-term financial security, the migrant path is more stable. You get access to healthcare, housing, and structured financial systems that support future wealth building.

Ultimately, the digital nomad lifestyle can save you more money short term, while the migrant lifestyle helps you build wealth long term.

Whether you choose to travel the world as a digital nomad or settle abroad as a migrant, both paths require careful planning and smart financial habits. There’s no one-size-fits-all answer — only what fits your goals, income style, and risk tolerance.

If you want to maximize your savings, learn to budget in foreign currencies, track expenses, and avoid lifestyle inflation. Both nomads and migrants can thrive financially if they stay intentional with money.

So before packing your bags or buying that ticket, ask yourself: Do I want flexibility or stability? Fast savings or steady growth?

The answer will determine not just how much money you save — but how you live your life abroad.